The European Union’s Corporate Sustainability Reporting Directive has fundamentally changed how businesses report on environmental, social, and governance performance. Understanding CSRD compliance is no longer optional for companies operating in or selling into European markets. It is a legal obligation with defined deadlines, specific reporting frameworks, and real penalties for non-compliance.

Whether your company falls directly under the directive or sits in the supply chain of a company that does, CSRD compliance will affect your operations, your data collection processes, and your reporting infrastructure. The corporate sustainability reporting directive applies to approximately 50,000 companies across the EU and extends its reach to thousands of non-EU businesses through subsidiary and revenue thresholds.

This article breaks down the six core CSRD compliance requirements that every company must understand, along with practical guidance on CSRD reporting standards, disclosure obligations, and implementation timelines. If your organization has not yet begun preparing for corporate sustainability compliance, the time to act is now.

1. Double Materiality Assessment

The first and most foundational CSRD compliance requirement is the double materiality assessment. Unlike traditional financial reporting, which focuses only on how external factors affect the company, CSRD requirements mandate that companies also assess how their operations impact people and the environment.

This means businesses must evaluate materiality from two directions simultaneously. Financial materiality examines how sustainability issues create risks and opportunities that affect the company’s financial position. Impact materiality examines how the company’s activities affect the environment, climate, workforce, and communities. Both perspectives must be documented and disclosed under the CSRD disclosure rules.

The double materiality assessment determines which topics a company must report on under the European Sustainability Reporting Standards. Not every company will report on every topic, but the assessment itself is mandatory. Companies that skip or superficially complete this step will fail CSRD compliance audits because the entire reporting structure depends on a rigorous materiality analysis.

For companies new to eu sustainability reporting, the double materiality assessment is typically the most resource-intensive requirement. It requires cross-functional input from finance, operations, legal, sustainability, and strategy teams. Organizations that have already implemented corporate sustainability compliance frameworks for other standards will find this process more manageable, but the CSRD’s dual-lens approach is more demanding than most existing frameworks.

2. Reporting Under European Sustainability Reporting Standards (ESRS)

The second critical CSRD compliance requirement involves reporting under the ESRS framework. The corporate sustainability reporting directive introduced these standards to replace the fragmented landscape of voluntary sustainability reporting with a single, mandatory, and auditable set of requirements.

ESRS covers multiple reporting areas organized into cross-cutting standards, environmental standards, social standards, and governance standards. Within these categories, companies must report on climate change, pollution, water and marine resources, biodiversity, workforce conditions, supply chain impacts, business conduct, and more, depending on the results of their materiality assessment.

What makes CSRD reporting standards particularly demanding is the level of granularity required. Companies must provide both qualitative descriptions of policies and practices and quantitative metrics with defined calculation methodologies. Vague sustainability narratives are insufficient. The CSRD disclosure rules require specific data points, targets, timelines, and progress measurements.

For companies that previously relied on GRI, SASB, or CDP frameworks, there is overlap but not equivalence. ESRS has its own structure, and CSRD compliance requires adherence to the ESRS format regardless of other frameworks a company may use. Aligning existing reporting with CSRD requirements typically requires a gap analysis to identify where current disclosures fall short.

3. Mandatory Third-Party Assurance

The third CSRD compliance requirement that distinguishes this directive from previous regulations is mandatory limited assurance by an independent third party. Under earlier reporting frameworks, sustainability disclosures were largely self-reported with no verification requirement. The corporate sustainability reporting directive changes this entirely.

Companies subject to CSRD compliance must have their sustainability reports audited by an accredited assurance provider. Initially, the requirement is for limited assurance, which is less rigorous than the reasonable assurance applied to financial statements. However, the EU has signaled its intention to transition to reasonable assurance as CSRD reporting standards mature and assurance methodologies develop.

This requirement has significant implications for corporate sustainability compliance. Companies must ensure their data collection processes, internal controls, and documentation standards are audit-ready. Assurance providers will examine not just the final disclosures but the underlying systems and processes that generated the data.

For businesses preparing for eu sustainability reporting, this means investing in data governance infrastructure well before the reporting deadline. Companies that wait until the assurance engagement to discover data gaps will face costly delays and potential CSRD compliance failures.

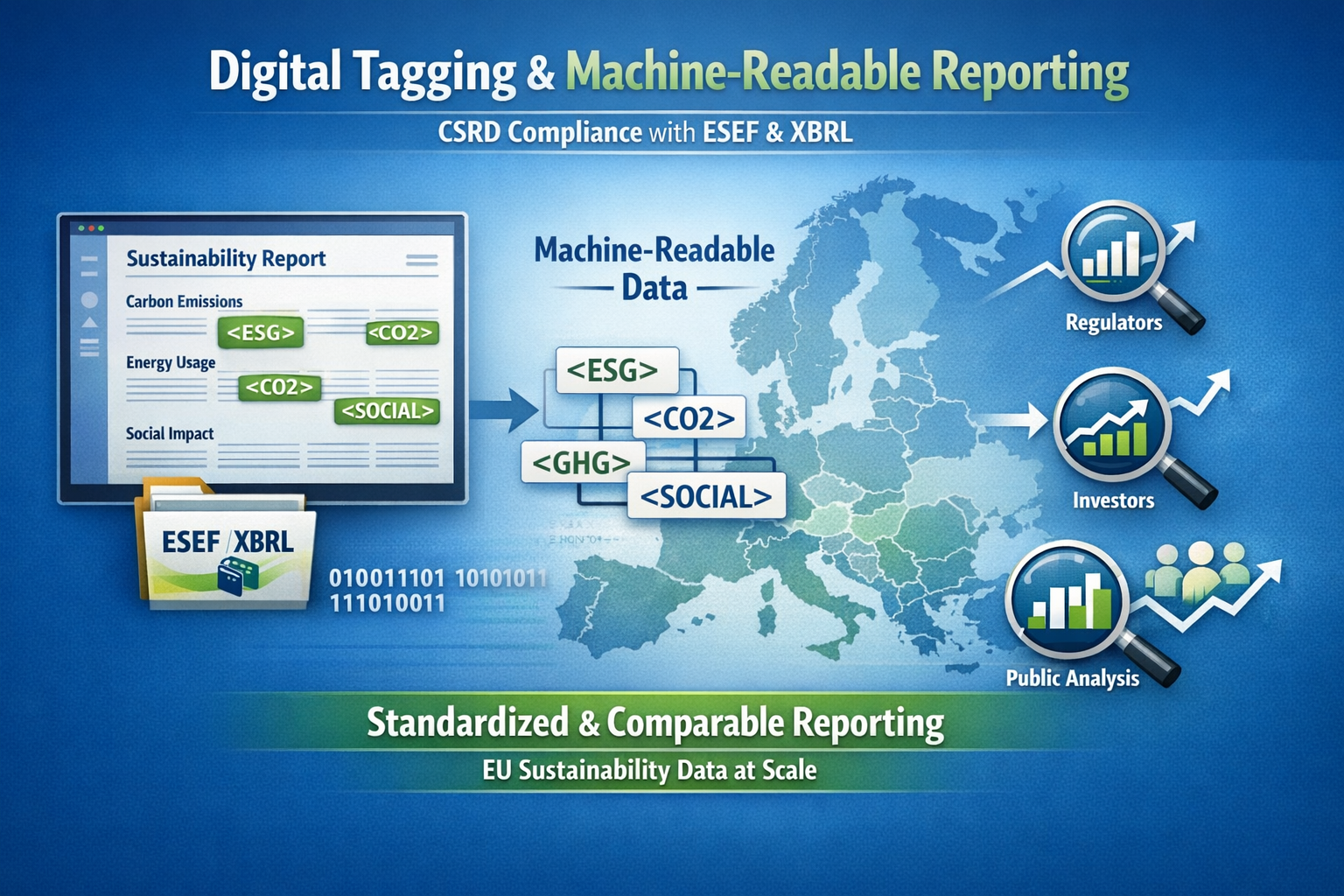

4. Digital Tagging and Machine-Readable Reporting

The fourth CSRD compliance requirement addresses how reports are formatted and submitted. The corporate sustainability reporting directive mandates that sustainability disclosures be digitally tagged using the European Single Electronic Format (ESEF) and XBRL taxonomy.

This is a technical requirement that many companies underestimate. CSRD disclosure rules specify that sustainability information must be machine-readable, enabling regulators, investors, and the public to extract, compare, and analyze data across companies and sectors automatically. This is a deliberate move toward standardized, comparable eu sustainability reporting at scale.

For CSRD compliance, companies need reporting software or service providers capable of producing XBRL-tagged sustainability disclosures. The tagging must align precisely with the ESRS data points, meaning every metric and disclosure element needs to be mapped to the correct taxonomy entry.

Companies that currently produce PDF-only sustainability reports will need to significantly upgrade their reporting infrastructure. This CSRD requirement is often the most technically complex for organizations without existing digital reporting capabilities, and it requires coordination between sustainability teams, IT departments, and external technology vendors.

5. Value Chain Reporting

The fifth CSRD compliance requirement extends reporting obligations beyond a company’s direct operations to include its entire value chain. Under CSRD requirements, companies must disclose material sustainability impacts, risks, and opportunities across upstream suppliers, downstream customers, and other business relationships.

This is where CSRD compliance becomes particularly challenging for large, complex organizations. Companies must collect, verify, and report sustainability data from entities they do not directly control. The CSRD reporting standards acknowledge this difficulty by providing a transitional period during which companies can use estimates and sector-level data where entity-specific value chain data is unavailable.

However, the expectation is clear: companies must progressively build the systems and relationships needed to collect actual value chain data over time. Corporate sustainability compliance under the CSRD is not a static exercise. It is a multi-year journey toward increasingly granular and accurate value chain transparency.

For businesses that serve as suppliers to CSRD-reporting companies, this requirement creates an indirect CSRD compliance obligation. Even if your company does not meet the direct thresholds, your customers may require you to provide sustainability data to fulfill their own CSRD disclosure rules. This ripple effect is one of the most significant aspects of the corporate sustainability reporting directive, effectively extending eu sustainability reporting requirements far beyond the companies directly subject to the law.

6. Integration with the Management Report

The sixth CSRD compliance requirement mandates that sustainability disclosures be published as a dedicated section within the company’s management report, not as a separate standalone document. This integration signals that sustainability information carries the same weight and governance oversight as financial information.

Under CSRD requirements, the board of directors bears explicit responsibility for the accuracy and completeness of sustainability disclosures. This is not a task that can be delegated to a sustainability department in isolation. CSRD compliance requires board-level governance, internal controls, and sign-off processes equivalent to those applied to financial reporting.

This integration requirement also means that sustainability and financial reporting timelines must align. Companies cannot publish sustainability data months after their financial statements. The corporate sustainability compliance framework under CSRD demands simultaneous preparation and release, which requires significant coordination between finance and sustainability functions.

For organizations that have historically treated sustainability reporting as a communications exercise rather than a governance function, this CSRD compliance requirement necessitates a fundamental structural shift. Sustainability data must flow through the same control environment, approval processes, and audit procedures as financial data.

How to Prepare for CSRD Compliance

Meeting these six CSRD compliance requirements demands a structured approach:

- Conduct a gap analysis comparing current reporting practices against CSRD requirements and ESRS standards to identify deficiencies.

- Invest in data infrastructure capable of collecting, managing, and tagging sustainability data at the granularity demanded by CSRD reporting standards.

- Engage assurance providers early to understand their expectations and build audit-ready processes before the first reporting cycle.

- Train cross-functional teams on CSRD disclosure rules so that finance, legal, operations, and sustainability functions collaborate effectively on corporate sustainability compliance.

- Map your value chain and begin engaging key suppliers and partners on data sharing requirements for eu sustainability reporting obligations.

Conclusion

The six CSRD compliance requirements outlined in this guide, spanning double materiality, ESRS reporting, third-party assurance, digital tagging, value chain transparency, and management report integration, represent the most comprehensive eu sustainability reporting framework ever implemented. These are not aspirational guidelines. They are enforceable legal obligations with defined timelines and penalties.

Companies that treat CSRD compliance as a strategic priority rather than a regulatory burden will gain advantages in investor confidence, supply chain positioning, and market credibility. The corporate sustainability reporting directive rewards organizations that build genuine corporate sustainability compliance capabilities, not those that treat it as a last-minute checkbox.

The CSRD compliance journey is complex, but the requirements are clear. The companies that begin now will be the ones best positioned when reporting deadlines arrive.

For more such information do visit us @CleanIndex